Long-Term Care Planning

Long-term care planning involves preparing in advance for the potential need for extended care services.

This process includes legal and financial strategies aimed at:

- Covering the high costs of nursing home or assisted living care

- Maximizing eligibility for public benefits

- Preserving assets for spouses and future generations

- Reducing financial and emotional stress on your family

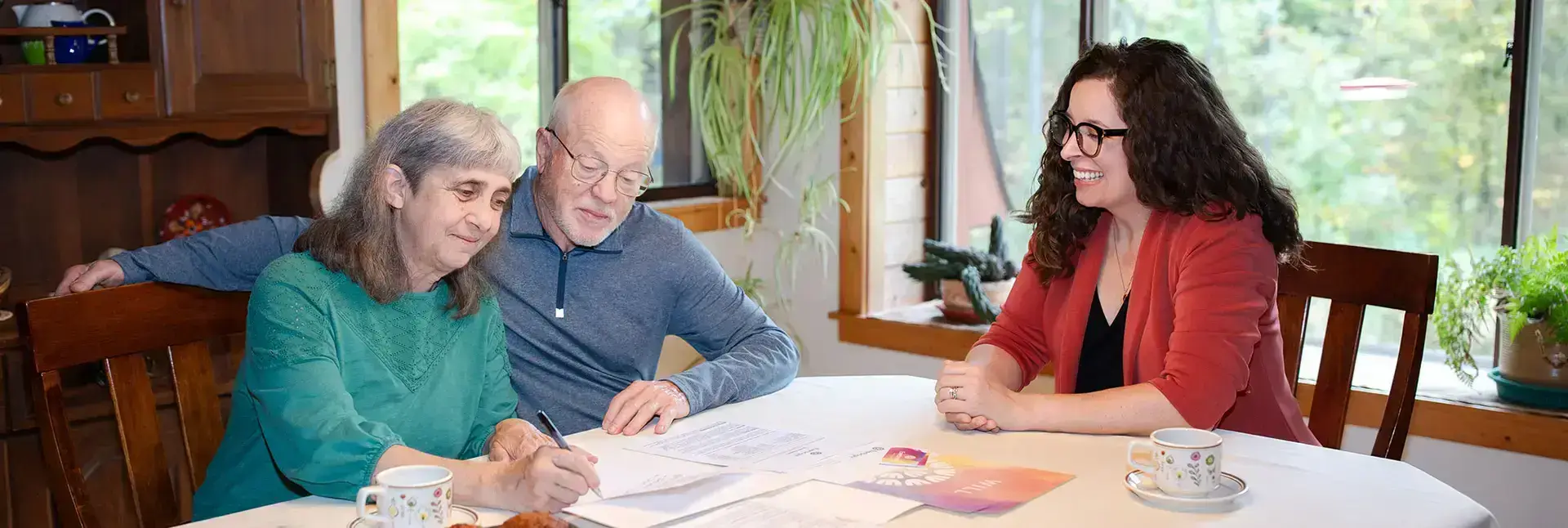

Our elder law attorneys work closely with you to create a personalized care plan that addresses your healthcare needs, financial goals, and legal protections.

A Need for All

As we age, many individuals face the need for long-term care due to chronic illnesses, disabilities, or the natural process of aging. The costs associated with nursing home care, assisted living, or in-home support can be overwhelming, often creating a significant financial strain on families.

At Everbright Legacy Law, we assist individuals and families in navigating these challenges through careful and strategic long-term care planning. Our goal is to protect your dignity, preserve your assets, and ensure you receive the care you need without depleting a lifetime of savings.

Key Areas of

Long-Term Care Planning

Medicaid (Medical Assistance) Planning

Medicaid is the primary government program that provides coverage for long-term nursing home care, but it has strict income and asset eligibility requirements. We assist clients with:

- Qualifying for Medicaid while preserving their assets

- Navigating complex look-back and transfer rules

- Completing and managing the Medicaid application process

- Developing spend-down and exemption strategies

Asset Preservation & Protection Strategies

We use legal tools to help clients protect their hard-earned assets while still qualifying for long-term care assistance. Our strategies include:

- Preserving the family home

- Providing spousal income and resource protections

- Planning for gifting and asset transfers (in compliance with Medicaid rules)

- Establishing caregiver agreements

- Avoiding unnecessary spend-downs

Irrevocable Trust Planning

Asset protection trusts can play a critical role in Medicaid planning by safely transferring assets out of your name before the look-back period, while still allowing you to maintain some control or benefit. We carefully structure trusts to:

- Comply with state and federal Medicaid laws

- Preserve eligibility for benefits

- Maintain control through thoughtfully designed trust terms

- Avoid probate and ensure legacy protection

Annuity & Income Planning

For some clients, Medicaid-compliant annuities can be utilized to convert countable assets into income for a healthy spouse. We guide clients through:

- Proper annuity structuring

- Ensuring regulatory compliance

- Coordinating with Medicaid rules

Veterans Benefits & Minnesota Veterans Homes

Many Minnesota veterans and their spouses may qualify for VA Aid & Attendance benefits or admission to a Minnesota Veterans Home. Our VA Accredited Attorneys help families:

- Determine eligibility for VA pensions and supplemental benefits

- Apply for VA Aid & Attendance

- Navigate the application process for Minnesota Veterans Homes

- Coordinate VA and Medicaid benefits for maximum coverage

Minnesota Veterans Homes provide high-quality long-term care for qualifying veterans. Understanding income limits, asset thresholds, and application procedures is essential for securing placement and benefits — and we are here to guide you every step of the way.

Who Needs

Long-Term Care Planning?

Long-term care planning isn’t just for the elderly or those currently facing health issues — it’s for anyone who wants to protect their future, their family, and their finances.

At Everbright Legacy Law, we work with individuals and families across Minnesota to create personalized long-term care plans that provide peace of mind and financial security.

You may need long-term care planning if you or a loved one:

Are approaching retirement

Preparing for the future means more than saving for travel or leisure — it means protecting your health, your independence, and your assets in case long-term care becomes necessary.

Have a chronic illness or diagnosis

Conditions like Alzheimer’s, Parkinson’s, MS, or other progressive illnesses can increase the likelihood of needing in-home care, assisted living, or nursing home placement. Early planning ensures that resources are in place when they’re needed.

Are a caregiver or family decision-maker

If you’re helping a parent, spouse, or other loved one plan for their care — or managing a crisis — legal and financial guidance is critical. We help families navigate benefits, protect assets, and make informed choices during difficult times.

Want to qualify for Medicaid or veterans benefits

Programs like Medical Assistance (Medicaid) and VA Aid & Attendance can help cover the cost of long-term care, but eligibility rules are complex. We help clients structure their finances and plan ahead to preserve assets while qualifying for support.

Are a veteran or the spouse of a veteran

You may be eligible for financial assistance or placement in a Minnesota Veterans Home — but the application process and asset rules can be daunting. We can help you understand your options and guide you through the process.

Own a home or significant savings

Without proper planning, the cost of long-term care can quickly deplete your estate. We use proven strategies — including trusts, annuities, and spousal protections — to help clients preserve their homes, savings, and legacy.

Frequently

Asked Questions

1. What types of long-term care services are available?

Long-term care can include a range of services such as in-home personal care, adult day care, assisted living facilities, memory care units, and nursing home care—each designed to meet different levels of medical and personal support.

2. How much does long-term care typically cost?

Costs vary widely depending on the type of care, location, and level of support needed. For example, in-home care may cost less than nursing home care, but all can be expensive over time without proper planning.

3. Can insurance cover long-term care expenses?

Long-term care insurance policies can help cover some costs, but not everyone has coverage, and policies often have limits or exclusions. Medicaid and Veterans Benefits often serve as important safety nets for many families.

4. How does Medicaid help with long-term care costs?

Medicaid (Medical Assistance in Minnesota) covers many long-term care services for eligible individuals with limited income and assets. However, qualification rules are complex, making early planning crucial to protect assets and qualify for benefits.

5. What is “spend down” and why is it important?

“Spend down” refers to reducing your countable assets to meet Medicaid eligibility limits. Proper planning ensures spend down is done strategically, protecting as much of your estate as possible.

6. Won’t the County tell me what to do with my assets?

When applying for Medicaid (Medical Assistance), the application is submitted to a county financial worker through the Department of Human Services. It’s important to understand that the role of the financial worker is not to provide advice on how to preserve or reduce your assets—they are tasked with determining eligibility based on the information you provide. In most cases, they will advise you to spend down your assets on care until you meet the financial limits for eligibility.

By contrast, an experienced elder law attorney can help you identify legal strategies to preserve assets, reduce unnecessary spend-down, and make informed decisions that align with your goals. With knowledgeable guidance, you can navigate the complex Medicaid process while protecting your financial security and your legacy.

7. Can I keep my home while receiving long-term care benefits?

Yes, with appropriate planning such as using trusts or other legal tools, it is often possible to protect your home from being counted toward Medicaid eligibility or estate recovery.

8. How does long-term care planning affect my family?

Planning can reduce the financial and emotional burden on family members, clarify care decisions, and help preserve your legacy for future generations.

9. What legal documents should I have in place as part of long-term care planning?

Essential documents include a will, durable power of attorney, healthcare directive, and potentially trusts—each serving to manage your finances, healthcare decisions, and asset protection.

10. When is the best time to start long-term care planning?

The sooner, the better. Early planning maximizes your options, helps protect assets, and avoids crisis-driven decisions.

11. Can I make changes to my long-term care plan over time?

Absolutely. Your care needs, finances, and laws can change, so ongoing reviews and updates are vital to keep your plan effective.

The Everbright Way

At Everbright Legacy Law, we take a different approach compared to traditional law firms that rely on hourly billing and limited-duration representation for long-term care planning.

We recognize that a diagnosis can bring uncertainty, difficult questions, and concerns about the future. That’s why we offer ongoing representation designed to support you every step of the way.

Our commitment is to walk alongside you, providing guidance, support, and clarity as you navigate the complexities of long-term care. Together, we help you make informed decisions that protect your well-being and preserve your legacy, ensuring your future remains bright.